Table of Contents

- What is an eCheck?

- Why eCheck Payments Make Sense for B2B Companies

- What CFOs Should Know About eCheck Payments

- How to Overcome Common Challenges with eCheck Payments

- Accept and Process eCheck Payments with Paystand

- Common Questions About eCheck Payments

Key takeaways:

- eChecks solve the B2B cash flow bottleneck by clearing faster than paper checks. This directly improves DSO and frees up working capital.

- The cost savings are substantial with eChecks. This eliminates hidden expenses from paper check processing and manual reconciliation.

- Implementation challenges like system integration, staff training, and internal approvals are manageable one-time hurdles.

- From a compliance perspective, eChecks operate under well-established NACHA regulations with clear liability frameworks. This makes them a low-risk payment method that CFOs can confidently approve.

Most B2B finance teams know the frustration: Paper checks sit in the mail for days, then take another week to clear, and stretch cash conversion cycles unnecessarily. Despite this impact on DSO, 75% of companies still use them.

Convincing customers to change their payment habits in a way that suits your receivables processes can be daunting. The trick is to find a happy middle ground that reduces customer complexity while increasing visibility on your end.

eChecks strike this balance by keeping the familiar check process while cutting clearing time to a few days instead of weeks.

For finance leaders managing working capital constraints, this timing difference translates directly into improved cash flow without forcing uncomfortable conversations about payment method changes.

What is an eCheck?

An eCheck (electronic check) is a digital version of a paper check that transfers funds directly from the payer's bank account to the payee's bank account using the Automated Clearing House (ACH) network.

The main difference between a paper check and an eCheck is speed—what used to take over a week now happens in days.

Think of it as digitizing the check without changing how customers interact with the payment. They still provide routing and account numbers, just like writing a check, but skip the physical mailing and deposit steps.

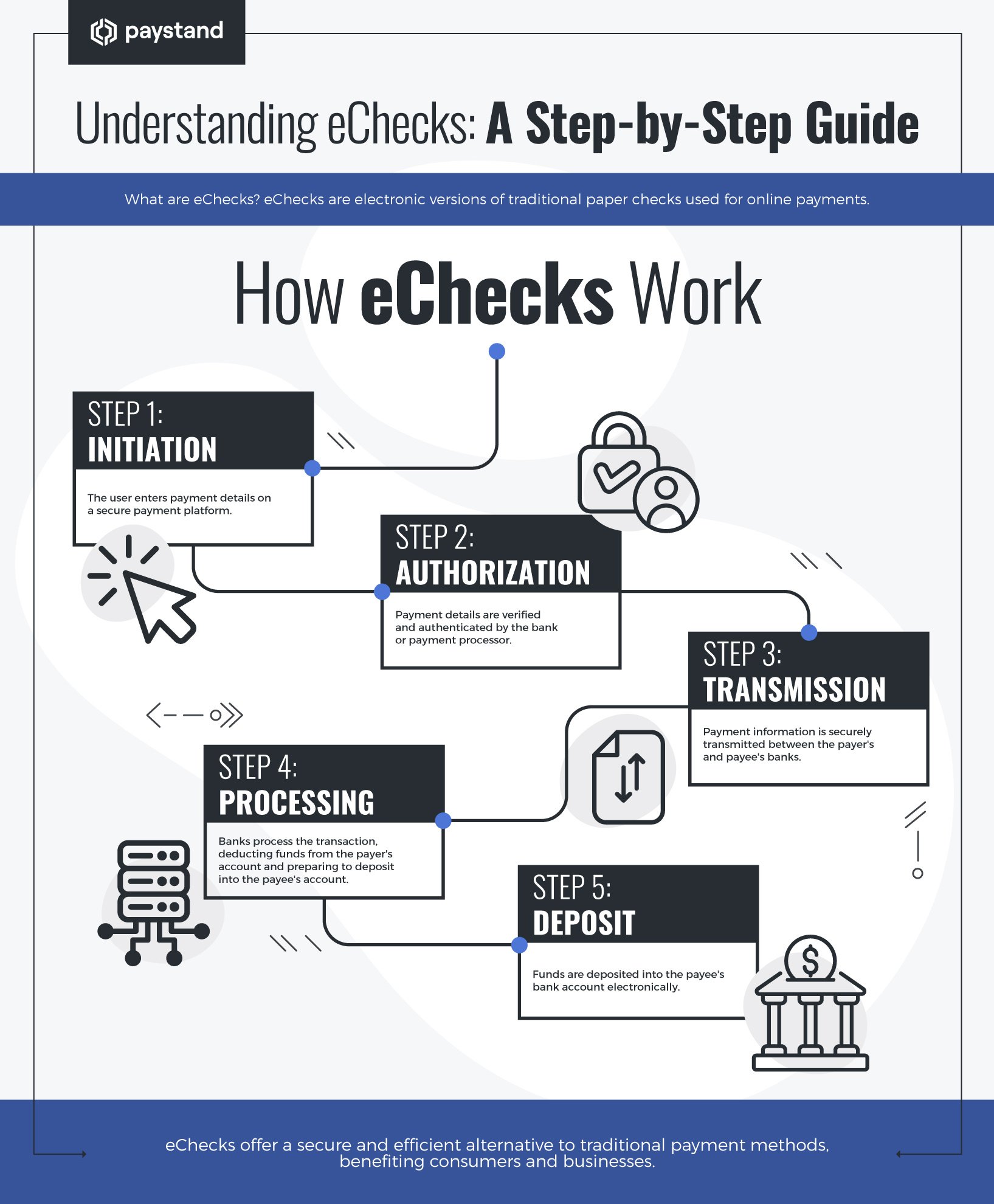

How do eCheck Payments Work?

The eCheck process starts when your customer receives an invoice with the eCheck payment option. They enter their bank details, including routing and account numbers, as they would on a paper check. After authorizing the payment, the system encrypts their data and sends it to your ACH processor.

Your processor validates the account information and creates an ACH debit entry, then submits it to the customer's bank for approval. The funds move through the Federal Reserve system to your bank account.

You get a settlement notification, and the transaction appears in your AR system for reconciliation.

The entire cycle takes 1-3 business days instead of the week-plus timeline you're used to with paper checks. No physical handling, no deposit runs, and no waiting for checks to clear.

eCheck Clearing Timelines and Cancellations

The speed difference between eChecks and traditional payment methods becomes clear when you compare processing windows and cancellation policies.

|

Payment Method |

Processing Time |

Cancellation Window |

Cancellation Process |

|

eCheck |

1-3 business days |

Before ACH processing begins (usually same day) |

Automatic notification, instant reversal |

|

Paper Check |

5-10 business days |

Before deposit (physical retrieval required) |

Manual process, potential delays |

|

Wire Transfer |

Same day |

Very limited (usually within hours) |

Complex reversal, fees may apply |

eChecks offer the best balance of speed and flexibility. You get faster clearing than paper checks with reasonable cancellation windows, unlike wire transfers, where changes become expensive quickly.

Why eCheck Payments Make Sense for B2B Companies

The operational benefits of eChecks extend beyond just faster processing. They create measurable improvements across your entire cash management workflow.

Faster Cash Flow and Reduced DSO

The math is straightforward: cutting four to seven days from your payment clearing cycle directly improves your days sales outstanding. For companies processing hundreds of thousands in monthly receivables, this timeline reduction translates to significant working capital improvements.

Consider a company with $500K in monthly check payments. Moving from 8-day to 2-day clearing frees up roughly $100K in working capital that was previously tied up in float. That's capital you can deploy for operations, growth investments, or to reduce reliance on credit facilities.

The DSO impact compounds over time. Better cash conversion cycles improve your ability to capture early payment discounts, negotiate better terms, and maintain stronger cash reserves for unexpected opportunities.

Lower Processing Costs Than Traditional Methods

Processing costs add up quickly when you factor in the full expense of handling paper checks versus eChecks. Paper check processing includes postage, deposit preparation time, bank fees, and the hidden cost of delayed cash access.

eChecks typically cost $0.25-$1.50 per transaction compared to $15-$50 for wire transfers. After factoring in the staff time saved from eliminating manual deposit processes, the cost differential becomes even more substantial.

The savings become more pronounced at higher volumes. A company processing 200 checks monthly saves roughly $2,000-$4,000 annually just on direct processing costs, before accounting for operational efficiency gains and improved cash flow timing.

Enhanced Payment Security and Fraud Protection

eChecks process through the established ACH network, which has built-in fraud monitoring and verification systems that paper checks can't match. Every transaction gets validated through multiple checkpoints before funds move, reducing the risk of fraudulent payments.

Paper checks are vulnerable from the moment they leave your customer's office until they hit your bank account. They can be intercepted, altered, or copied. eChecks eliminate these physical vulnerabilities by keeping all payment data encrypted and transmitted directly through secure banking networks.

The ACH network also provides liability frameworks and dispute resolution processes. When issues arise, you have documented transaction trails and established procedures for resolution, unlike the often murky process of tracking down paper check problems.

Simplified Reconciliation and Reporting

Digital transaction data flows directly into your AR system, eliminating the manual data entry that comes with processing paper checks. Each eCheck payment includes detailed transaction information that automatically matches to outstanding invoices.

Your accounting team spends less time reconciling payments and more time on analysis. The electronic trail provides complete audit documentation without the need to store and manage physical check copies.

Monthly and quarterly reporting becomes more accurate because payment data is captured consistently and completely. You get better visibility into payment patterns, customer behavior, and cash flow trends when all the data is structured and searchable.

Customer Payment Flexibility Without Complexity

eChecks work with existing customer bank accounts, removing the need for new registrations, apps, or account setups. Customers provide the same routing and account numbers they'd write on a paper check, just through a secure online form instead of physical mail.

The familiarity reduces customer resistance while improving your cash flow. You're not asking customers to learn new systems or change their fundamental payment approach, just streamline the delivery method.

This balance helps maintain customer relationships while improving your operational efficiency.

You avoid the friction that comes with pushing customers toward unfamiliar payment methods while still capturing the benefits of electronic processing.

Reduced Administrative Burden

Eliminating physical check handling removes manual steps from your payment processing workflow. No more sorting mail, preparing deposits, or making bank runs. Your team can focus on exception handling and customer service rather than routine processing tasks.

The time savings compound across your finance organization. AR staff spend less time on data entry, bank reconciliation becomes more straightforward, and month-end closing processes move faster when payment data is already digitized and organized.

Administrative efficiency improvements often exceed the direct cost savings. When your team spends less time on manual processing, they can focus on more strategic activities like cash flow forecasting, customer relationship management, and process optimization.

What CFOs Should Know About eCheck Payments

Financial executives need to understand the regulatory and risk framework around eChecks before implementation. Fortunately, eChecks operate within well-established banking regulations with clear compliance paths.

Regulatory Framework and NACHA Compliance

eCheck payments fall under NACHA's ACH network rules. These aren't experimental regulations but established banking standards that have governed electronic payments for decades.

NACHA sets clear requirements for transaction authorization, data security, and dispute resolution. Your payment processor handles most compliance obligations, but you need to ensure proper customer authorization and maintain transaction records according to NACHA standards.

Penalties for non-compliance typically involve transaction fees and processing restrictions rather than severe financial penalties. The regulatory risk is manageable when you work with established payment processors who understand NACHA requirements and build compliance into their systems.

Data Security and Financial Liability

Bank account information requires the same protection standards as credit card data, but the liability framework is more straightforward. ACH transactions have clear rules about unauthorized payments and dispute resolution timelines.

Your payment processor should meet PCI compliance standards and provide data encryption for all bank account information. Most established processors carry insurance coverage for data breaches and unauthorized transactions, reducing your direct financial exposure.

Look for clear indemnification clauses that protect your company from losses due to processor security failures, while ensuring you meet your obligations for customer authorization and data handling.

Audit Requirements and Documentation Standards

eCheck transactions create comprehensive audit trails automatically. This documentation typically exceeds what's available for paper check processing.

External auditors expect consistent record retention and clear documentation of internal controls around payment processing. eCheck systems provide structured transaction data that supports SOX compliance requirements and simplifies audit preparation.

Transaction records must be retained according to banking regulations, typically seven years for ACH payments. Most processors provide automated record retention and reporting tools that meet these requirements without additional administrative burden on your finance team.

Risk Management and Insurance Considerations

eCheck fraud liability is generally lower than credit card chargebacks, but you should understand your exposure to NSF fees and unauthorized payment disputes. Most processors provide fraud monitoring and will flag unusual transaction patterns.

Review your existing business insurance to ensure adequate coverage for electronic payment processing. Some policies may need updates to cover ACH payment risks, though coverage gaps are typically smaller than those associated with credit card processing.

Indemnification clauses in processor contracts are critical. Look for agreements where the processor assumes liability for security breaches and unauthorized access, while you maintain responsibility for proper customer authorization and compliance with your internal controls.

How to Overcome Common Challenges with eCheck Payments

Here's how you can navigate the most common obstacles finance teams encounter when implementing eChecks in their companies:

-

Complex system integration and technical setup: Evaluate API capabilities early and focus on processors with pre-built ERP integrations rather than custom development. Plan for a 30-60 day implementation timeline with parallel testing to resolve compatibility issues before going live.

-

Staff training and workflow change inertia: Start training two to three weeks before implementation with hands-on practice rather than theoretical sessions. Assign eCheck champions within each team to become subject matter experts who can support colleagues during the transition.

-

Internal approvals and compliance workflow design: Build your business case around measurable cash flow improvements and established regulatory frameworks rather than theoretical benefits. Engage IT, legal, and finance stakeholders early with specific documentation about security standards and compliance requirements.

-

Exception and error management complexity: Establish clear escalation procedures and response timeframes for common eCheck issues like NSF payments and processing errors before going live. Create standardized communication templates for customer outreach during payment exceptions to maintain consistency and professionalism.

-

Volume and transaction limit management: Work with your processor to understand daily and monthly ACH limits that could impact high-volume operations. Plan payment batching strategies for large invoices that might exceed individual transaction limits, and establish backup processing schedules during peak payment periods.

Accept and Process eCheck Payments with Paystand

Partnering with a comprehensive payment platform can address implementation challenges while maximizing cash flow benefits for your organization.

Here's how Paystand simplifies eCheck payments:

-

Fixed processing: Save thousands monthly compared to credit card processing with Paystand's micro fixed fee structure rather than percentage-based pricing. This cost model becomes increasingly advantageous as your transaction volumes grow.

-

Instant funds verification and ERP integration: Seamlessly integrate with major ERP systems for streamlined AR workflows while providing real-time account validation. Support for 90% of U.S. banks ensures broad customer compatibility without friction.

-

Smart Check technology for digital transition: Bridge paper and digital payments with Smart Check's scan-and-process capability that digitizes physical checks instantly. Customers can scan, edit, and submit check information in seconds while you get automated reconciliation and faster deposits.

-

Automated recurring payments and mobile processing: Enable subscription-style B2B payments and mobile check processing through enterprise-level APIs. Customizable implementations support large-scale operations with the flexibility to adapt to specific workflow requirements.

Ready to reduce your DSO by transitioning to eChecks? Explore Paystand's eCheck solutions today.