.webp "Enhance Business Efficiency with ERP Payment Solutions")

As more business transactions move online, the need for front- and back-end system integrations grows. Traditional fund-transfer methods can be challenging, error-prone, and costly. The answer? An enterprise resource planning ERP payment system.

According to a Cybros report, 77% of SMEs reported that their ERP helped them standardize back-office processes. The same report showed that this tool also helped optimize spending by 11%. Since we specialize in online payments, we know how much an integrated payment solution can improve ERP software. This guide will cover the basics of ERP payment gateways and portals, including their benefits and cautions. It will also provide a blueprint for future usage in your company.

What is an ERP System?

ERP stands for enterprise resource planning and refers to a type of software management system that organizations use to run their everyday operations. These include accounting, supply chain, procurement, manufacturing, project and risk management, employee benefits, and all other aspects of human resources, financials, compliance, and operations. ERP systems can also include enterprise performance management: tools that allow businesses to effectively strategize, budget, and conduct reports on all financial activity.

How do ERP Systems Work?

- ERP systems allow every sector of your company to operate from a single database. They are designed to decrease the number of resources your business needs to run efficiently while still helping ensure profitability.

- ERPs collect essential information from different parts of the enterprise and categorize it all under one centralized location. In this way, they help businesses escape the "information silos" – a phenomenon that can occur when information is not collected correctly and passed from one business segment to another.

- ERP systems use automation to collect information and then deliver that information to the areas of the business that need access to it the most. For example, suppose a direct-to-consumer business is running low on inventory, and a shipment order has been made for some of the last items in stock. In that case, the ERP's inventory management sectors will take note of this and inform the departments in charge of restocking inventory that they need to restock soon. The sales and marketing teams will also be informed so that they can pause selling and advertising items that are currently not in stock.

What are the Different Types of ERP Systems?

There are a few different types of ERP systems available. Knowing the differences among them is vital so that you can choose the best option for your company's needs:

- On-premise ERP systems. This type of ERP software is deployed on the premises of the specific business using it. Because this kind of ERP system is usually entirely controlled by the enterprise it's linked to or the ERP consultant, it's usually used by businesses prioritizing security. However, implementing this type of ERP application requires dedicated, on-prem IT resources that can handle tasks such as application and server maintenance. This kind of ERP system is also highly customizable and can be integrated seamlessly into your existing systems.

- Cloud-based ERP systems. Cloud-based ERP systems are also known as SaaS products, and a third-party service manages them. Cloud-based ERPs have flexible designs that give teams easy access to critical company data. While this type of ERP system requires you to trust a third-party vendor with some of your sensitive data, the upside is that it doesn't require the same financial investment or specialized team needed to purchase an on-prem system.

- Hybrid ERP systems. Hybrid ERP systems are also known as two-tier ERP systems. They allow your company to combine on-prem ERP system technology with cloud technology. For companies that want to gain access to the expertise of ERP consultants without sharing highly secure company information with a third party, hybrid ERP systems are an excellent investment.

History and Evolution of ERP Payments: a Timeline

- 1960s - Manufacturing Resource Planning (MRP) systems emerge, focusing on managing manufacturing resources.

- 1979 - Credit card terminals mark the beginning of electronic payment systems.

- 1990s - Enterprise Resource Planning (ERP) systems exist, expanding on MRP by incorporating accounting and other business functions.

- 2000s - ERP systems integrate with external payment systems, improving financial transaction management performance.

Development of Payment Gateways

- 1979 - Credit card terminals are introduced, marking the early stages of electronic payment systems.

- Post-Internet Era- Payment gateways emerge as alternatives to traditional credit card processors, connecting merchants and customers using new technologies.

- 2000s - Payment gateways have become more sophisticated, integrating better, encrypting, and storing data locally.

Challenges in B2B Transactions

Despite advancements in payment systems, B2B transactions face challenges due to negotiated terms, varying discounts, proprietary legacy systems, and complex accounts receivable workflows.

Adoption of Integrated Electronic Payment Options

- The introduction of Internet transactions, enabling electronic credit cards and ACH payments for online shopping, shifts the consumer market.

- B2B transactions lag in adopting integrated electronic payment options due to complexities in contracts and workflows.

Integration of ERP with Payment Systems

- Businesses realize the benefits of integrating ERP software with external payment systems to enhance performance.

- Integrated payment solutions and gateways supplement ERP accounting modules, improving efficiency in managing financial transactions.

What is an ERP Payment?

An ERP payment is a financial transaction initiated, managed, or facilitated through an ERP system. Organizations use these platforms to manage various operations, including finance, accounting, human resources, supply chain management, etc. ERP payments aim to enhance efficiency, accuracy, and transparency in financial transactions within an organization.

In ERP, payments typically involve:

- Generating invoices

- Processing purchase orders

- Managing customer payments and accounts payable

- Disbursing funds to vendors or suppliers

ERP systems streamline these payment processes by integrating them with other functions, automating tasks, and providing visibility and control over financial activities.

ERP payments can encompass various payment methods, including:

- Checks

- Bank transfers

- Credit cards

- ACH and EFT transfers

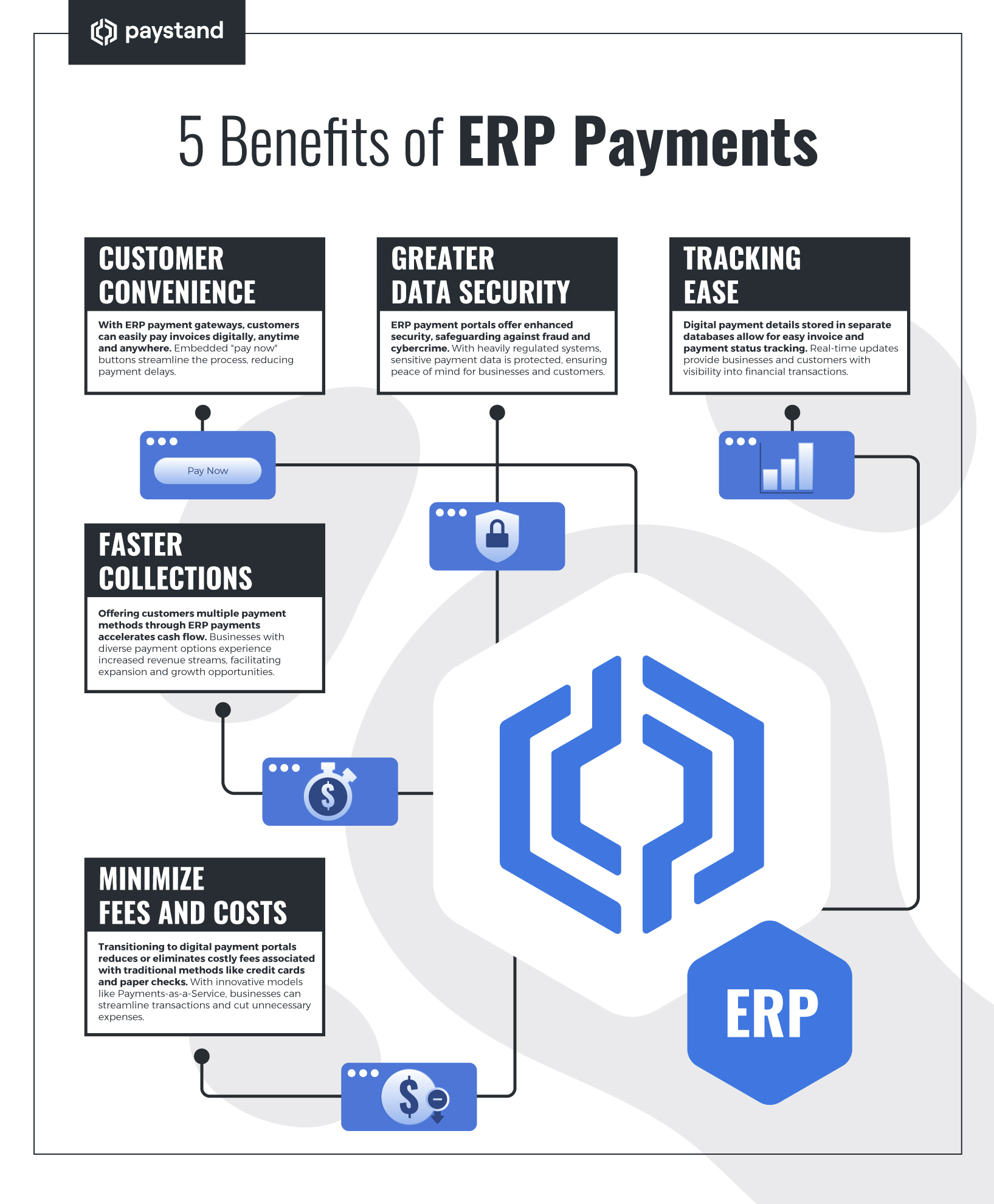

What Are the Main Benefits of ERP Payment Gateways and Portals?

Customer Convenience

One of the most significant advantages of an ERP payment gateway is making it easy for customers to pay invoices. Customers can easily make a digital payment anywhere and anytime once an invoice is received. Businesses can eliminate payment delays by integrating a portal with embedded "pay now" buttons.

Greater Data Security

Digital B2B transactions are safer and more accessible to track than paper-based systems. This helps organizations avoid fraud and cybercrime. Payment portals are generally heavily regulated to protect sensitive payment data.

Tracking Ease

Digital payment details are stored in separate databases so businesses and customers can track invoice and payment status in real time.

Faster Collections

Businesses can collect money faster by offering customers different payment methods. Merchants with more payment options made seven times more money than those without. This dynamic leads to better cash flow and more resources available for expansion and growth.

Minimize Fees and Costs

Credit card use incurs expensive fees, and processing paper checks requires much effort. Companies can reduce or eliminate these costs by transitioning to digital payment portals. Many payment methods, especially paper checks, include fees and soft charges. For example, Paystand helps businesses eliminate transaction fees through a Payments-as-a-Service model.

What Are the Potential Risks of ERP Payment Gateways and Portals?

Businesses should carefully select payment gateways, even though ERP gateways offer many advantages. Here are some considerations:

- Fraud Risk. Although digital payment portals are regulated and secure, cybercriminals can target them. To avoid security risks, portals with strong security protocols are crucial.

- Compliance Requirements. Financial institutions have increased their rules and regulations to keep money movement safe. This relates to the security issues mentioned earlier. Ensure your payment portal solution stays up-to-date and complies with all these regulations on your behalf.

- Integration Investment. Integrating ERP systems with payment portals and gateways is easier now. However, it still requires resources to ensure compatibility, especially with older legacy systems.

- High Customer Expectations. Today's customers are trained to buy various consumer goods online, pay quickly, and take possession of those items within a day or two. That expectation is moving its way up the supply chain, adding pressure on B2B companies to overcome the challenge.

The Paystand Advantage

Paystand aims to reboot commercial finance and create a more open financial system, starting with B2B payments. Integration with ERP systems is a primary part of that mission.

Paystand is a robust, state-of-the-art payment-as-a-service provider that offers payment gateways into ERP systems. It has years of experience and uses SaaS and blockchain technology, making it efficient and secure. Here are some key features of Paystand's ERP payment gateway.

Variety of Payment Options

Paystand allows customers to accept all major credit and debit cards, ACH, and direct bank payments with a single integration. Businesses can quickly receive customer payments without adding extra work or processes, making it more convenient to handle accounts receivable. When customers click Paystand's "pay now" button in emails, invoices, or sales orders, they will be redirected to a payment portal. From there, they can choose their preferred payment option.

Lower Costs in Accepting Different Payments

As a value-added service, Paystand has worked with processors to secure wholesale processing rates with no extra fees. Additionally, using least-cost routing tactics can reduce payment processing costs. This is done by transferring extra fees to the end consumer when they select a higher-fee payment method.

Subscription Payment Options

If you have a subscription-based business product, that feature can cause problems in the AR process. Paystand's ERP gateway allows these organizations to collect flexible subscription payments more efficiently. Managing custom pricing, different billing intervals, and repeat payments is simple and efficient.

Virtual Terminal

Companies can safely receive payments over the phone, in person, or by mail using a secure virtual terminal. This terminal securely transfers information to the ERP system. Paystand's flexibility can make payment collection even simpler and more efficient.

The Paystand Bank Network

Working with Paystand has a significant advantage: its Bank Network helps companies avoid transaction fees. Over 140,000 businesses use this Bank Network for direct payments, saving thousands in fees.

Tokenization Process

Merchants can save customers' payment methods securely with Paystand. It encrypts and vaults the information using tokenization. This converts sensitive data into a token that only works within a specific system. Best practices are then used to store, audit, authenticate, and authorize credit card payments. This process is more secure than encryption because a token cannot be mathematically reversed into usable data.

PCI DSS Compliance

Paystand is a PCI DSS-certified payment processor. The system creates a safe network and protects cardholder data. It also has a program to manage vulnerabilities and implement access controls. Additionally, it regularly monitors and tests networks and has an information security policy.

Multiple Integrations

Paystand offers integrations with various ERP systems to streamline businesses' payment processes. While the specific list of supported ERPs may evolve, some of the commonly integrated ERP systems with Paystand include:

These integrations enable seamless connectivity between Paystand's payment solutions and ERP platforms, allowing businesses to manage their financial transactions more efficiently and securely.

ERP and payment portals have evolved over the past several decades. Now is the perfect time to thoroughly combine these technologies. ERP payment systems and portals can help businesses save money, increase cash flow, grow, and succeed. Ready to discover everything Paystand can do for your business? Subscribe to our newsletter and keep track of our latest developments.