As online transactions become more prevalent, the payment process has become more complex. For finance teams, it's about payment options and partnering with the right online merchant service providers.

Cashless payments are projected to double by 2030, especially in the United States, where digital payments in B2B transactions are expected to reach $1.5 trillion by 2024. B2B organizations must invest in their payment infrastructure for better visibility and cash flow.

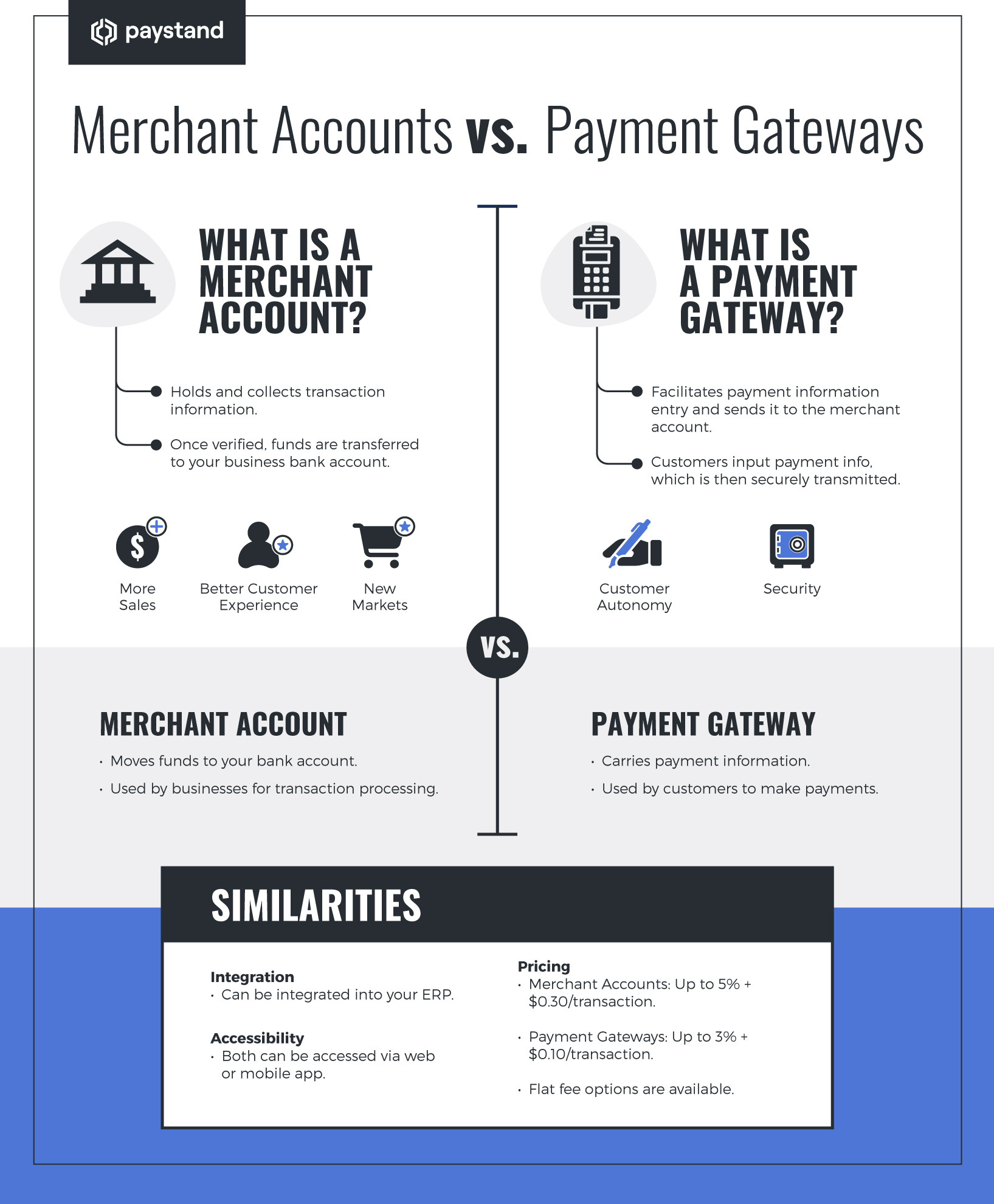

The process begins with selecting a payment gateway and merchant account.

What is a Merchant Account?

A merchant account holds and collects transaction information. Once the information is verified, the funds are passed to your business bank account. Think Stripe or PayPal.

Merchant accounts are mandatory for accepting credit card payments. There are several benefits to investing in a merchant account, such as:

- More sales

- Better customer experience

- Tap into new markets, including international customers

What is a Payment Gateway?

The payment gateway is how payments are brought into your platform. It's where customers check out and add their payment information, which is then sent to the merchant account.

The benefit of having a payment gateway is that customers can fill out payment information themselves. Depending on the solution, the payment portal will likely be secure and compliant, which mitigates the risk of fraud.

Is a Payment Gateway the Same as a Payment Processor?

Payment gateways and payment processors are different, even though they are similar. While a payment gateway sends the initial payment information to the merchant account, a processor connects with all the networks and moves the money.

A payment processor is a mainstay of Point-of-Sale (POS) systems and doesn't necessarily require a payment gateway.

However, as more businesses use virtual terminals for in-store and online purchases, the trend is to use both for a seamless experience.

What is the Difference Between a Merchant Account and a Payment Gateway?

The easiest way to categorize the two is that a merchant account moves funds, and a payment gateway carries information. Both are required to process credit card and debit card transactions.

Businesses use merchant accounts to move transactions into their business bank account. However, the end customer uses a payment gateway to pay for a service or product.

Both do have some similarities, however:

- For pricing, both services take a percentage with an additional fee for each transaction. Merchant accounts take up to 5% with a +$0.30 charge, while payment gateways can cost up to 3% + $0.10 per transaction. However, some vendors will have flat fee rates.

- Both can often be accessed via the web or mobile app.

- You can integrate your merchant account or payment gateway into your ERP, depending on your solution.

What to Look for In a Payment Solution?

Many options can help you determine which payment solution is right for your business. These are features to consider outside of their integration with your other applications:

- Budget. Flat fee pricing is often better than individual transaction fees. Consider the potential savings.

- Security. Use secure encryption and fund-on-file tokenization.

- Usability. The interface must be intuitive for the finance team and customers.

- Payments Network. Ensure the provider has a vast bank network and can process payments from all major card issuers.

- Strategic Features. Look for features like ACH incentives, convenience fees, and payment automation.

- Enhanced Data. The solution should provide end-to-end visibility into the payment process.

Take Your Payments to the Next Level

We've uncovered the nuances regarding payment gateway, merchant account, and everything else. Now, it's time to elevate your business.

Often called the Venmo of B2B transactions, Paystand is an end-to-end payment solution that can process just about any payment option—checks, eChecks, ACH, credit cards, debit cards, bank-to-bank transfers - you name it. With our seamless invoicing and "pay now" functionality, your customers can effortlessly and securely send and store payment information. We also integrate with all major ERPs, including NetSuite, Sage Intacct, WooCommerce, and Xero.

Clients have seen up to 60% decreases in DSO, 50% in savings on account receivables, and more.

Find out if our platform meets your needs in a short customized demo today.