Online B2B payment platforms have the substantial advantage of offering customers many payment methods. However, two stand out regarding security, convenience, and cost-effectiveness: wire transfer and direct deposit.

These two payment options have so much in common that it's easy to confuse them. The similarities are stark, as each is a mode of electronic funds transfer that deals directly with financial institutions. However, understanding the differences can help you and your AR team determine whether direct deposit payments or wire transfers make the most sense for your business.

What is a Wire Transfer?

A wire transfer is an electronic transfer that sends money from one bank account to another. Individuals and businesses commonly use international wire transfers to send money to other parties overseas. Until the advent of credit cards and digital wallets, bank transfers were the most secure method of cross-border business. However, that's changing rapidly as other payment methods become more widespread and affordable.

This type of money transfer isn't limited to international business. You can also make a domestic wire transfer.

Despite the annual volume of wire transfers declining by 4% between 2021 and 2022, this remains a crucial digital payment option.

How Do Wire Transfers Work?

Most financial institutions offer wire transfer services, with traditional banks and credit unions being the most common facilitators of money transfers. These providers allow transfers over the phone, an online portal, or an in-person branch.

Issuers can also use a non-bank provider, as these services may be cheaper or more convenient.

Wire transfers require the sender to provide a government-issued identification and the following information:

- Issuer's bank account number

- Recipient's full name and contact information

- Recipient's bank account and transit number

- Recipient's bank name, address, and phone number

Issuers must read the fine print before sending the wire transfer. Federal law grants all senders the right to know all taxes, exchange rates, and fees. You may also find domestic and international wire transfer instructions on your financial institution's website.

Wire Transfers Pros

There are a few reasons why wire transfers haven't faded into obscurity. Here's a look at the top pros for this money transfer method:

- Velocity. Most recipients can access funds within a few hours. They may have to wait about two business days for international wire transfers. However, turnaround times are still much faster than other methods of sending money overseas. Furthermore, there is an audit trail because these are essentially bank transfers.

- Easy currency exchange options. Wire transfers make it easy to send money in a currency that is not your local one. Most services will offer to exchange it, but you must pay the associated fees.

- Safety. Wire transfers go through the Office of Foreign Assets Control, which ensures that those involved in terrorist activities or money laundering don't receive the money.

Wire Transfers Cons

Wire transfers are great, but there are a couple of downsides to consider:

- High costs. Not surprisingly, there's a price to pay for the convenience of wire transfers. Fees vary for this digital payment option depending on the provider or method used (online, over the phone, or in person). Money sent within the U.S. will cost around $35, and international transfers can cost $50 in fees.

- Irrevocability. Once a wire transfer is sent, the transaction cannot be reversed. Therefore, the recipient's details must be correct on the form.

What is a Direct Deposit?

A direct deposit, sometimes called an Automated Clearing House (ACH) payment, is another quick way to make electronic payments. However, this method has significant differences from a wire transfer. First, an ACH transaction is typically a domestic payment. This is because an ACH transfer uses a specific, US-based ACH network. It's common for businesses to use an ACH payment for payroll. However, as the technology and infrastructure behind the ACH system have improved, this form of money transfer has become standard across the payment landscape.

How Do Direct Deposit Works?

Direct deposits rely on the ACH Transfer System, a U.S. banking network that facilitates transactions between financial institutions. Banks, credit unions, and the Federal Reserve are all part of this network, making direct deposits accessible.

Direct Deposit Pros

Among the many advantages direct deposits provide, we can find the following:

- Affordability. Direct deposits are much more affordable than wire transfers, as banks allow recipients to receive their funds for free. Businesses must pay system implementation fees, but they're nothing compared to the cost of sending frequent wire transfers. The medium cost for an ACH payment in 2022 was between $0.26 to $0.50 per transaction.

- Convenience. Depositing paychecks directly is much easier than dealing with the hassle of manual labor paper checks. It's also quicker and, of course, safe.

- Safety. Direct deposits are safe because they arrive directly into your bank account. With checks, you have to consider the possibility of fraud.

Direct Deposit Cons

Two disadvantages of direct deposit to keep in mind include the following:

- Slowness. Direct deposits are the slowest payment method, taking one to five business days.

- Possibility of insufficient funds. When a paycheck or payment enters your account, it's easy to assume it will always be added to your account automatically. However, reviewing your bank account regularly is vital to ensure the correct direct deposit payment.

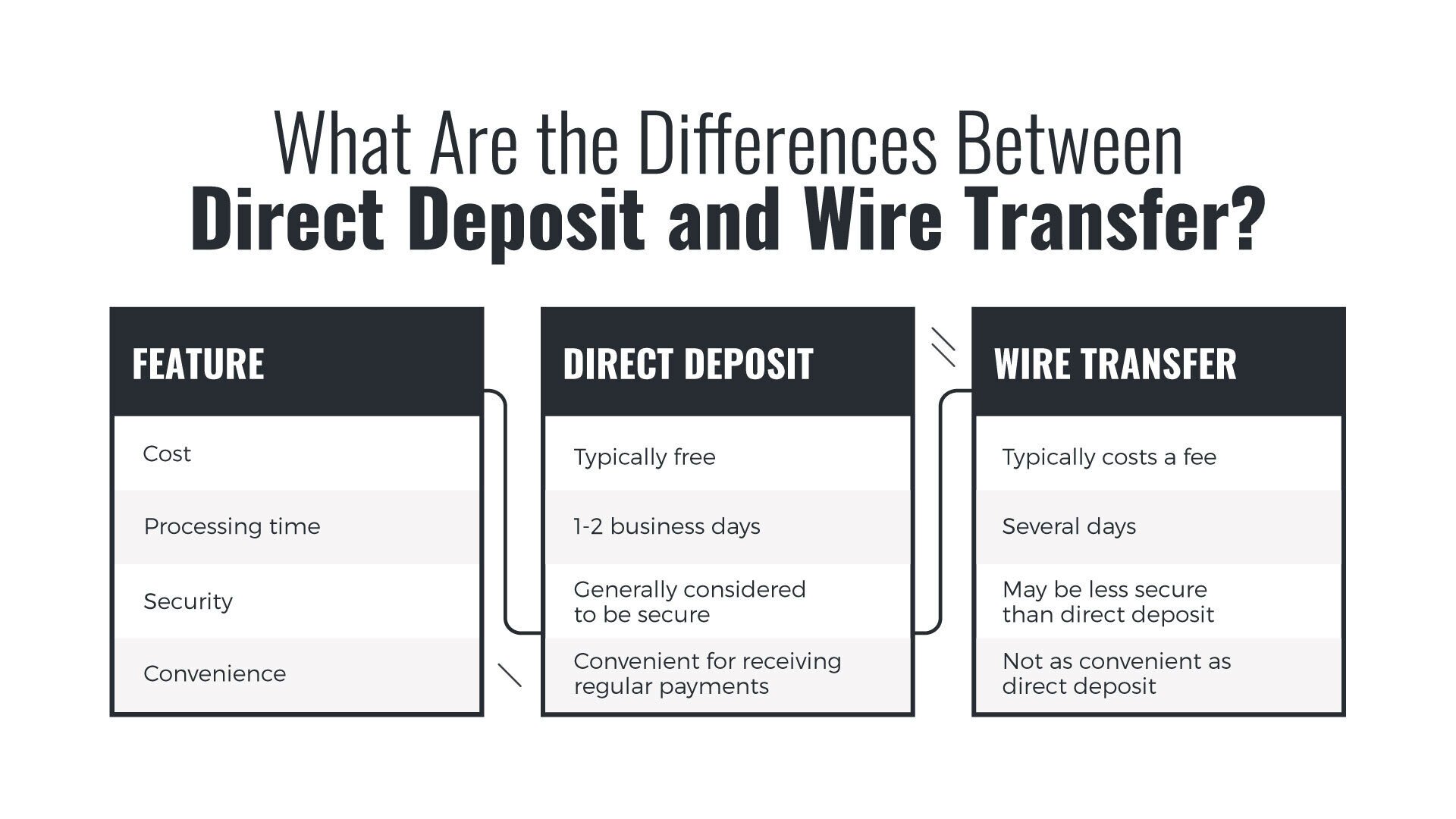

What Are the Differences Between Direct Deposit and Wire Transfer?

Direct deposit and Wire transfer are both methods of electronically transferring money, but there are some key differences between the two. Here is a table summarizing the key differences between direct deposit and wire transfer:

Which method of electronic funds transfer is right for you depends on your needs. Direct deposit is the most convenient and cost-effective option if you receive regular payments. A wire transfer may be best if you send or receive a large amount of money. Here are some additional things to keep in mind when choosing between direct deposit and wire transfer:

- Direct deposit is the most secure method of electronic funds transfer. Your money is deposited directly into your bank account, so there is no risk of being intercepted.

- Wire transfers can be less secure than direct deposit. If you are sending a wire transfer, be sure to use a reputable financial institution and take steps to protect your personal information.

- Direct deposit is the most convenient method of electronic funds transfer. Your money is deposited directly into your bank account, so you don't have to worry about going to the bank to cash a check.

- Wire transfers are not as convenient as direct deposit. You have to go to the bank to initiate a wire transfer, which can take several days to receive the money.

To make a decision, evaluate these four aspects of each digital payment method: cost, speed of receipt, limit, and security. Both processes involve costs on the issuer's and recipient's sides.

If you use wire transfers and direct payments, each client's needs call for a specific solution. Paystand supports these transactions and has a zero-fee processing option, the Paystand Bank Network, streamlining payments for you and your clients.

If you enjoyed this article, we're thrilled to inform you that you can read more about B2B payments, AR automation, and exciting payment news in our monthly Newsletter. Subscribe now!